The personal loan foreclosure means closing your ongoing personal loan account with your lender after paying the remaining outstanding amount.

Personal loans carry higher interest charges, and borrowers don’t want to pay extra charges over a longer tenure.

Hence, when they have sufficient money, they want to close their personal loan accounts and save on interest costs.

It is where the personal loan foreclosure helps them. Read on and know about the personal loan foreclosure procedure!

Personal loan foreclosure procedure at a glance

Make a visit to the lender that you have availed the personal loan with.

Carry proof of identity, loan account number, bank passbook displaying that you have paid EMIs. Also, carry a cheque for making the prepayment.

For availing the personal loan foreclosure, the lender may ask you to pay the penalty, which could be 3-4% of the remaining principal amount.

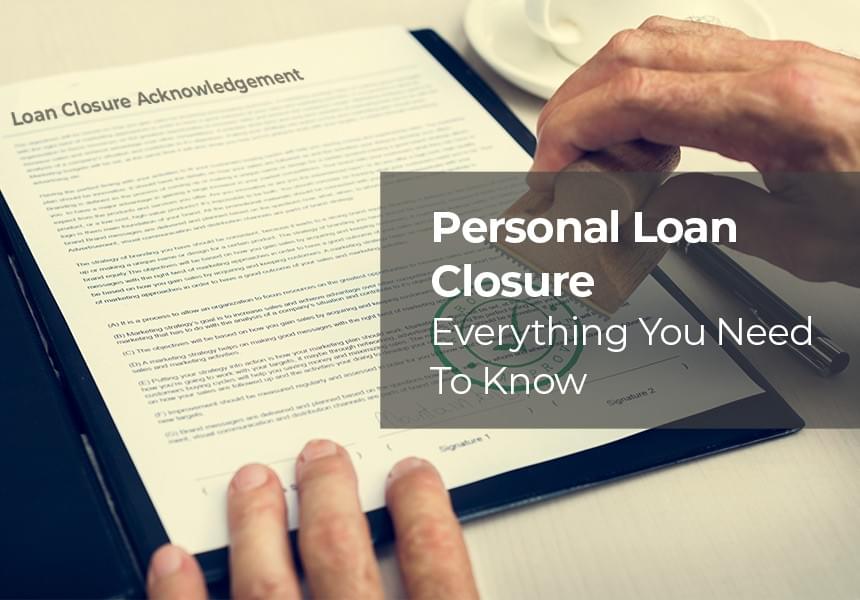

After you settle the entire loan, along with the penalty charge, a letter of acknowledgement may be issued to you. You should keep it for future references.

Some lenders may also issue you a No Dues Certificate (NOC).

These are only the standard procedure for personal loan foreclosure. The personal loan foreclosure may differ from lender to lender. Hence, the best thing is getting in touch with your loan provider to know about the precise foreclosure steps.

The benefits of going for the personal loan foreclosure are that you can save on extra interest charges as well as become debt free. Now, when you clear off your debt before time, you can fulfil your next goal with another loan.

Bajaj Finserv presents to you pre-approved offers on personal loans and much more. It can simplify your loan processing to make it hassle-free.

You can share your basic details like your name and mobile number and check out your pre-approved loan offers now.